Just when we thought the impact of COVID-19 had a detrimental impact on the future of Australia’s foodservice sector, the recent announcement of Woolworths intention to acquire 65% shareholding of PFD Foodservice (*pending regulatory approval from the ACCC) poses a series of strategic challenges for manufacturers, suppliers and competitors in the food and beverage industry.

While there are many operational synergies that Woolworths Australia can leverage to maximise and recover their investment in PFD quickly (E.g. logistics, supply chain, back office systems and processes, etc.), there are also hidden upsides to Woolworths in this transaction that could pose a risk to both suppliers and competitors as a result of the impending majority shareholding in PFD.

Who is PFD Foodservice?

PFD Foodservice is reportedly Australia’s largest privately-owned foodservice distributor. According to their website (https://www.pfdfoods.com.au/about-us) PFD’s reach in non-grocery channels is extensive and includes:

PFD has an estimated turnover in excess of $2 billion, servicing 39,000 foodservice customers through 68 distribution centres, via a fleet of 750 delivery vehicles with more than 200 sales representatives in trade.

With Woolworths gaining bolt-on access to a wide variety of channels and customers this begs the question; what are the potential costs and ramifications for Woolworths suppliers and competitors as a result of the PFD acquisition?

From our assessment there are four areas Woolworths can seek to leverage its acquisition of PFD that could have significant impacts on its suppliers and competitors:

-

- – Trading Terms

- – Increased buying power leading to cheaper purchase price of goods

- – Channel diversification and reach

- – Leveraging suppliers outside the Grocery Code of Conduct

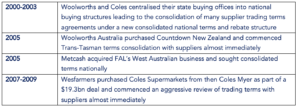

A repeat pattern of Trading Terms consolidation

Historically, one of the first areas Australia’s grocery retailers and wholesalers have sought to benefit financially from acquisitions is through supplier trading terms. Over the past 20 years a clear repeat pattern of this behaviour exists:

As an employee of various suppliers during these events, I was either a witness to, or participant in, each of these negotiations. I can attest to the rigorous approach applied by the retailers in each instance.

Consolidation of trading terms is a means for the acquiring business (in this instance Woolworths) to leverage optimal trading rebates from suppliers which can lead to significant ongoing financial benefit almost immediately. This can lead to significant cost pressures on suppliers and a clear competitive advantage for the retailer.

Typically, supplier trading terms are modelled very differently in the foodservice sector than grocery. Most often the trading terms values are far lower in the foodservice sector which is reflective of the different product type/mix, cost structures, trading environment and operating model required to service foodservice customers.

Any such consolidation of terms across grocery and foodservice suppliers has the potential to place even greater cost pressure on suppliers and further shift the share of net profit available in Woolworths and PFD’s favour.

Increased size and scale often equates to increased buying power and cheaper prices

The scale of such an acquisition and the resultant increase in reach across multiple channels (coupled with back office efficiencies) poses significant risk to the many suppliers and competitors that must not be overlooked, nor should its value and impact be understated.

Complimentary to any rebates or trading terms benefits Woolworths and PFD may receive is the anticipated effect on its purchase prices. Should Woolworths seek to consolidate or streamline its pricing by applying pressure on suppliers, it could conceivably further enhance its competitive position in both the grocery and foodservice markets.

Any purchasing benefits achieved from the consolidation of supplier pricing has the potential to significantly impact supplier profitability. Such a benefit also has the potential to detrimentally impact competitors within the $11 billion foodservice sector (and other wholesale channels) as well. Competing in a market with a stronger price position than its competitors would afford PFD a distinct advantage.

Leveraging scale and reach

Consider this… Woolworths has in excess of 900 supermarkets that all begin operating as satellite distribution centres for its foodservice division. Seem radical? Well it isn’t. Woolworths already applies this model for its online grocery sales. Imagine in excess of 1,000 PFD distribution centres and Woolworths stores capable of delivering to foodservice customers across the country within 24 hours. It is a distribution reach that would rival Australia Post and potentially far more efficiently.

Then consider the non-foodservice channels that PFD already serves such as Petrol and Convenience stores. It is not inconceivable that Woolworths would target supplying the highly lucrative channel with a blend of impulse products such as confectionery, salty snacks and beverages in addition to PFD’s ‘Fresh to Go’ products.

With grocery buying prices and trade terms already secured for many of these product categories, offering a consolidated buying offer to corporate and independent convenience retailers is not a far-fetched notion. When you factor in the 2018 purchase of Hollier Dickson’s who already distributed to many of these customers, the skillset and sector knowledge already exists in the PFD business. It would stand to significantly impact the foothold of competitors in the convenience channel.

There is also the opportunity for Woolworths to leverage PFD to become a more comprehensive ‘one stop shop’ through the inclusion of liquor products to customers in the HoReCa channel (hotels, restaurants and cafes) and beyond. The Endeavour Drinks Group division of Woolworths already has access to a large assortment of beer, wine and spirits at best-in-market prices, as well as a healthy portfolio of private label brands which they could use to offer a simple all in one solution to thousands of customers.

Such a scale would pose a significant risk not only to suppliers but also the many privately owned and independent distributors who service these customers and channels. This would potentially place many small businesses and jobs at risk of being lost to the Woolworths juggernaut.

Operating outside Australia’s Grocery Code of Conduct

With so many means to extract value, profit and growth outside of the grocery sector, the risk is that trading pressures could be applied to suppliers who do not comply to the demands asked of them. In 2015 the Australian Grocery Code of Conduct was introduced to ensure fair and equitable negotiations occurring between suppliers and their major grocery customers.

The purpose of the Australian Grocery Code of Conduct was “…to deliver more contractual certainty in trading relations between suppliers and supermarkets, encourage the better sharing of risk and reduce inappropriate use of market power across the value chain.

The Code sets out clear obligations to ensure key elements of Grocery Supply Agreements are discussed and agreed up front. It does not seek to impose overly restrictive rules on commercial negotiations, but rather provides commercial flexibility within a set framework of requirements and controls on behaviour.”[1]

Should the position as majority shareholder of PFD be approved by the ACCC, over time Woolworths could develop many avenues for negotiation outside of the Grocery Code of Conduct that have the potential to have far reaching implications.

So what does this mean?

In 1999 Anthony Dimasi was commissioned by Woolworths Australia to qualify their market share based on overall household expenditure. This report evaluated Woolworths market share as a percentage of “total retail food and grocery spending”[2] which included groceries, liquor, restaurants, cafés, etc. to find that Woolworths Australia was only 20% of the total Australian household food and grocery expenditure at the time. 20 years on from that report it appears that Woolworths is making a concerted effort capture markets outside of its traditional grocery footprint.

To be clear, Woolworths has every right to attempt to secure its majority shareholding of PFD. Equally, the ACCC has the right to decide whether or not this move is fair, reasonable and in the best interests of all concerned.

Some have already raised their concerns including Countrywide CEO Richard Hinson who on the 19th August 2020 stated “Woolworths’ expansion of their B2B business at this time is nothing less than aggressive and opportunistic behaviour at a time when thousands of family-owned food distribution businesses and manufacturers across the country are struggling to keep their heads above water.”[3]

Should the acquisition be allowed to proceed, Woolworths has the potential to leverage its considerable portfolio across multiple channels, which could result in significant changes to customers, competitors and suppliers. There are likely several more long-term strategic opportunities Woolworths have and will identify to fully benefit from any such investment.

The responsibility of suppliers and competitors of both Woolworths and PFD is to identify the risks and opportunities that may come in future. Once identified, a clear strategy and action plan should be implemented immediately to mitigate any risks and capitalise on such opportunities.

The big winners during the COVID-19 pandemic (if they can really be called ‘winners’) have been the major grocery retailers. While the majority of food businesses have been hamstrung by necessary restrictions to prevent the spread of the Covid virus, consumers have had little choice but to flock to supermarkets. The result has been catastrophic for foodservice businesses and a significant weakening of their business health and market position.

When we consider this and the potential risks outlined in this article, is now the right time to be allowing Woolworths such a significant investment in PFD?

[1] Source: https://www.afgc.org.au/industry-resources/food-and-grocery-code-of-conduct

[2] https://www.aph.gov.au/binaries/senate/committee/retail_ctte/report/c04.pdf

[3] https://www.afr.com/companies/retail/woolworths-buys-552m-stake-in-pfd-food-services-20200819-p55n7x